Chaque jour nous vous présenterons une nouvelle Startup française !

Notre pays regorge de talents et d'entrepreneurs brillants ! Alors partons à la découverte des meilleures startup françaises ! Certaines d'entre elles sont dans une étape essentielle dans la vie d'une startup : la recherche de financement, notamment par le financement participatif (ou crowdfunding en anglais). Alors participez à cette grande aventure en leur faisant une petite donation ! Les startups françaises ont besoin de vous !

Bitcoin’s 10th anniversary will fall on Jan. 3. As a decentralized currency that belongs to everyone and no one, there is no official way to commemorate its 10th birthday. From wallet manufacturers to developers, every ecosystem participant will have their own suggestions as to how bitcoiners should mark the historic occasion.

Unofficial Ways to Celebrate Bitcoin’s Unofficial Birthday

It’s human nature to see significance in numbers. That’s why the crypto community lost its mind over a block hash containing 18 consecutive zeros earlier this year, and it’s also why there will be great fanfare over Bitcoin’s 10th birthday, despite the fact that numerically speaking, 10 is no more significant than any other integer.

It’s fitting that the cryptosphere can’t even agree on the official date of Bitcoin’s birthday, which could fall on Jan. 3, when Satoshi mined the genesis block, or on Oct. 31, when he published his whitepaper. For those who believe it to be the former (or simply want an excuse to celebrate Bitcoin’s birthday twice a year), there’s no shortage of ways to mark Jan. 3. Here’s how various ecosystem participants will be celebrating the event.

Merchants and Manufacturers

Vendors would predictably like you to celebrate Bitcoin’s 10th by buying memorabilia. We’ve covered much of this stuff already, including an expensive watch, an expensive clock, and a reasonably priced hardware wallet. For those too penurious or too cynical to rinse $4,000 on a Bitcoin timepiece, there are more affordable souvenirs available; a t-shirt or framed print should suffice.

Mainstream Media

Mainstream media have gotten cryptocurrency wrong for a decade, and they’re not going to break the habit of Bitcoin’s lifetime on its 10th. Expect buttloads of verbose hit pieces masquerading as thought pieces pondering “What has Bitcoin actually achieved?” By the time they finally get it, it’ll be too late. Meanwhile, don’t give the media the rage clicks they crave. If you really want to read about Bitcoin’s decade in review, there’ll be plenty of cryptocurrency publications, news.Bitcoin.com included, on hand to do the honors.

Mainstream media: still struggling to understand Bitcoin

Bitcoin Users

On Jan. 3, a significant number of bitcoin users will be busy withdrawing their cryptocurrency from exchanges and storing it on non-custodial wallets. The move will be initiated as part of Proof of Keys, a scheme designed to return ownership of bitcoin from third parties to individuals, where the digital coins were always meant to reside.

Bitcoin Developers

Expect to see plenty of geeky tweets from prominent Bitcoin developers on Jan. 3 that draw upon the rich trove of data at their disposal. A handful of devs have been working on the cryptocurrency’s code since the early days, and thus Bitcoin’s 10th will also be an opportunity for self-reflection. There are no longer service medals to be earned for making code commits to Bitcoin Core or Bitcoin Cash — merely the satisfaction that comes from knowing you’ve played a small part in optimizing Satoshi’s creation for the next wave of users.

Bitcoin Businesses

Exchanges, wallet developers, P2P platforms and other crypto businesses will be celebrating Bitcoin’s 10th in their own way; expect to see discounts, zero-fee trading and other offers to mark the occasion, plus a whole lot of Bitcoin trivia shared on social media.

While there’s no obligation to celebrate Bitcoin’s birthday (as a permissionless creation, that’s one of its charms), many of those who’ve come to know and love the cryptocurrency over the last 10 years will take a moment to toast this milestone. Whether that means raising a glass, buying bitcoin, or withdrawing coins to a non-custodial wallet, there are numerous ways to observe Bitcoin’s most symbolically significant birthday yet. The next time an anniversary as widely celebrated arrives will likely fall on Jan. 3, 2059, when Bitcoin turns 50. Here’s to the next 40 years.

How will you celebrate Bitcoin’s 10th birthday? Let us know in the comments section below.

Images courtesy of Shutterstock and Google Inc.

Need to calculate your bitcoin holdings? Check our tools section.

Holders of Bitcoin Cash (BCH) at social trading and multi-asset brokerage platform Etoro will now be compensated with a fiat cash amount of BSV corresponding to their pre-fork holdings. The decision comes six weeks after the contentious hard fork took place.

U.S.-based investment platform Etoro announced on Dec. 27 that customers who were holding BCH leading into the hard fork last month will be given a cash amount per BCHSV. The platform said it made the decision to do so, despite being “not obligated to support forks.”

Clients of the platform who held long non-leveraged BCH positions on Nov. 15 will receive credit into their accounts. “We are in the process of crediting relevant users’ accounts with the dollar value of BCHSV coins at a price of $92 multiplied by the number of BCH units held at the time of the fork,” Etoro said in an announcement.

Mati Greenspan, a senior market analyst at Etoro, told news.Bitcoin.com: “As a custodian holding the coins on behalf of our clients we felt that this was the best thing to do. Ideally we would want to give them the BCHSV itself because it belongs to them. But that would be very difficult to setup as we have not yet been able to add BCHSV to the platform.”

He said that Etoro was looking into adding BSV to its platform but added: “We have a lot of evaluation and technical considerations involved in adding a new asset to the platform.”

Etoro added that it had so far received an “extremely positive” response from its clients following the announcement. “The decision to send out the compensation was made in retrospect and we thought it would be a nice surprise for the holiday,” added Greenspan.

The Victorious Coin

The contentious Nov. 15 BCH network hard fork saw the blockchain split into two – BCH ABC and BCHSV. ABC was declared the dominant chain following the hard fork by securing more more proof-of-work than the BCHSV side following the the split. It has since kept the original BCH title on most major exchanges.

Over the course of 2018, failing initial coin offerings that raised billions last year have continued to dominate the news cycle. Despite ethereum losing more than two thirds of its value, ICO projects have been liquidating massive amounts of ETH. ICO treasuries cashed out 433,000 ETH ($52.4M) in December, surpassing every other month this year.

After Ethereum’s Price Dropped 84%, ICO Treasury Withdrawals Increased

One of the biggest stories of 2017 was how initial coin offerings (ICOs) raised billions. 2018 was a different story, with the recurrent themes being regulatory action against ICOs and the majority of these projects failing miserably. In February, research by news.Bitcoin.com revealed that over 46 percent of 2017’s ICOs had failed. Seven months, ago ICOs had a failure rate of 92 percent, showing the world that even though a project can raise millions it won’t necessarily go on to be successful. Furthermore, many of the ICOs trying to survive the 2018 bear market have been cashing out large amounts of ETH from their treasuries. Diar Research details that 433,000 ETH was withdrawn from ICO treasuries this month despite the fact that ETH’s value hit record annual lows in December.

“Ethereum has dropped 84% in price from the start of the year when ICO treasuries saw massive activity with withdrawals being the highest they ever were this year,” explains the chart created by Diar Research.

The researchers also detail that November (290,000 ETH withdrawn) was the second largest withdrawal period this year. Diar states that Tezos withdrew 82,000 ETH and Aragon moved 40,000 into the Ethereum stablecoin dai. The third highest month was in January, which saw a total of 232,000 ETH withdrawn from ICO treasuries. “As a whole, 24 percent from the start of the year has moved from the 100 wallets assessed — But what was worth $3 billion is now only $350 million,” explains Diar.

Out of 50 ICOs, Filecoin Cashed out Close to Half of the Month’s Treasury Withdrawals

Diar has shared a comprehensive spreadsheet which details 50 of the highest grossing ICOs and how much money they started with in January and how much they withdrew in 2018. Big name projects such as Digixdao, Polkadot, Golem, Tezos, and Filecoin are included in Diar’s informative table alongside treasury account holdings. Statistics show that Filecoin withdrew its entire stash of 216,906 ETH this December, which encompasses about half of the month’s total withdrawn coins. A few other projects also liquidated their entire treasury accounts this year and some projects have very little ETH left.

The research also explains that 2018’s average withdrawal rate was only about 2.4 percent, but December exceeded most months with 12 percent. Of course, withdrawing coins doesn’t necessarily mean the project failed, but that the team may have tried to avoid ETH’s volatility by using a stablecoin or converting to fiat. However, if they did convert to a stablecoin or some form of fiat then they would have gotten more bang for their buck if they cashed out earlier. It is strange that many of the projects withdrew the most ETH during November and December when ETH was at its lowest price range of the year. When these projects were faced with a burn rate that outpaced the funds on hand, they may have been left with no other choice.

What do you think about ICOs cashing out the most ETH during the months of November and December? Let us know what you think about this subject in the comments section below.

Images via Shutterstock, and Diar Research.

Want to create your own secure cold storage paper wallet? Check our tools section.

Martina spent over 20 years as a marketing and product executive building and crafting strategies for market-defining software like Microsoft Office and Netscape Navigator. As an operating partner at Costanoa Ventures, she sits on multiple boards and advises companies on all things go-to-market. She also teaches at the UC Berkeley graduate school of engineering.

Jim Wilson Contributor

Jim is a seasoned sales executive with over 25 years experience in diverse technology industries. As an operating partner at Costanoa Ventures, Jim provides companies with sales and market entry strategy advice.

There is a prevailing belief that the magic formula for early-stage tech startups hinges on how quickly they achieve $1 million in annual recurring revenue (ARR). Investors in SaaS companies, in particular, are very guilty of pushing this or its equally loaded corollary, “When will you sign your first six-figure deal?”

But in the rush toward these numbers, too many startups lose sight of their primary intent: These metrics are supposed to be an indicator of product/market fit. We’ve seen companies reach $1 million in ARR in less than a year, yet not have enough market momentum to get their next million easily. We’ve seen early-stage companies so concerned about getting those first sales, they don’t validate the market and if they’re building the right product. We’ve also watched a focus on new logos make companies forget about keeping existing customers happy, introducing unexpectedly high churn — something startups can’t afford.

Those first customers and that first million are supposed to be the bedrock on which the rest of the business grows. Founders must constantly ask what they’re learning about their market, product and go-to-market approach — in that order! — so the business becomes a flywheel.

Revenue is a lagging indicator of sales success, so must likewise be prioritized accordingly. That’s not to say revenue isn’t vitally important and that there isn’t a great deal of urgency to it, but focusing on it too much too early can mask big problems that will hurt startups later when the stakes are higher.

Here are a few lessons we’ve learned by watching our early-stage companies go through this crucial phase. Every early-stage company needs to do them well.

Customer and market discovery is job No. 1

We talk about product and knowing customers a lot, but that is insufficient. Startups must understand the market, as well. How do customers do this today? Is there urgency around the problem? What is the community saying? An early investor in PagerDuty went onto Reddit and Quora and just looked at who people were talking about. It made his decision easy.

To be really successful, it is as important to understand market dynamics as it is to deliver a great product. This also helps zero in on all the aspects of your ideal customer profile; it needs to be more specific than you think! This also then helps qualify customers for future sales.

Elevate Security stood out in their super-crowded security space because they carved out a unique position around people-powered security. They used their early sales process to carefully qualify who would help them best develop their products. Their first product got shout-outs on social media from users who loved it — a rare occurrence in security — and were indicators they had found good initial customers and were creating something unique.

Build a product that sells itself

You’ll always find smart people saying, “I love what you’re doing.” Some things are so broken even a mediocre improvement is worth a change. But this is why revenue can be a false indicator for scalable success: Founders find enough early adopters to get that first million, which leads them to believe the product is enough. The company starts chasing more revenue, not investing in a product-based growth engine. If sales keeps hitting their numbers, everyone believes things are fine. Until they’re not. And then it’s usually a really heavy lift, with 6-12 months of product, sales or team upgrades.

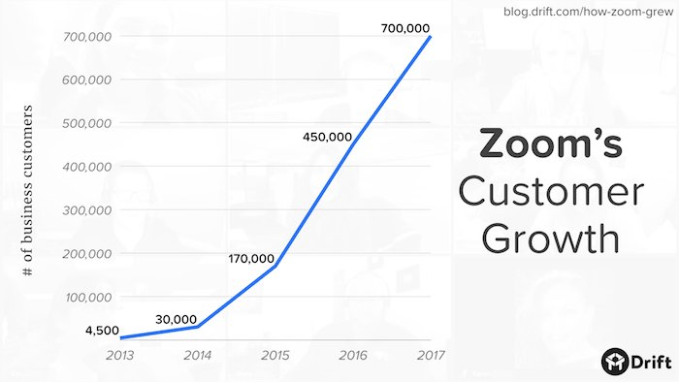

What startup doesn’t want a growth curve like this? Zoom had triple-digit growth for the last four years in a crowded, mature video conferencing category. Janine Pelosi, Zoom’s head of marketing, said the reason they were so successful before and after she arrived was they have a great product. It’s reliable, easy to use, and the founder, Eric Yuan, was selling it every day. Yuan knew the market really well coming out of Webex, and always touching customers meant he could adjust company strategy accordingly. Zoom embodied the real magic formula: know your market + build great product.

Pay attention to customer engagement and delight

Customer satisfaction is simple: It comes from the perception that people get value from their purchase; it’s much less about how much they paid. It’s also always cheaper to make an existing customer happy than it is to acquire a new one, so make sure even in the early days that you’re investing in making current customers happy advocates.

Aquabyte uses computer vision to identify sea lice in the $160 billion aquafarming market. When they showed customers FreckleID (think racial recognition for fish) to uniquely identify fish in a pen of 200,000, fish farmers loved the idea. The price they were willing to pay was 3x what the CEO thought possible. They’re likewise investing heavily in making sure their initial customer is successful with the product and are delighting them in unexpected ways (handwritten holiday cards). They have more prospects in their pipeline than they have capacity, which means they don’t need to expand sales to grow revenue fast.

Your startup may have the coolest tech, be in the biggest market and have the smartest team. No matter what your board says, remember revenue is NOT the primary indicator; it is simply an indicator. To become a breakout success, you need to read the tea leaves of all aspects of your market and build a product and customer experience that is truly superior.

from Startups – TechCrunch https://tcrn.ch/2ThiFrf

It’s been almost a decade since the inception of Bitcoin, a technology created by the infamous and anonymous Satoshi Nakamoto. Over the years, many people have been hunting for Bitcoin’s inventor and Satoshi sightings have increased a great deal since 2016. During the course of 2018 there were numerous so-called Satoshi sightings and a couple of individuals who claimed to be the mysterious creator himself.

2018 was a crazy year for cryptocurrency enthusiasts and a prolific one for all the loons who claimed to be Satoshi Nakamoto. A bunch of individuals came out of the woodwork this year to tell the world they created Bitcoin, and one of them even published the first chapter of a purported Satoshi Nakamoto autobiography. Then there were a few odd Satoshi-related sightings like the ‘21e8’ bitcoin hash, which actually led people to believe Satoshi was an alien time traveler with the ability to utilize superior quantum computation. Each and every story and self-proclaimed Satoshi failed to sway the crypto community in 2018, but nevertheless, the discussions revolving around Bitcoin’s creator remained as fun as ever.

The hunt for Satoshi Nakamoto in 2018 was filled with many debunked self-identifications and so-called sightings.

Satoshi’s Tell-All Book

This summer, bitcoiners found out that Satoshi Nakamoto was allegedly writing an autobiography. Back in June, Bloomberg columnist Matthew Leising led a few gullible people to believe that Satoshi was possibly writing his memoirs in order to publish a tell-all. A website called Nakamotofamilyfoundation.org, which has since been deleted, was a 21-page PDF of the first chapter. The website’s creators even added a cryptogram puzzle so curious readers could find some more ‘clues’ after solving.

“Announcing the first excerpt to a literary work consisting of two parts and the excerpt is provided — I wanted to include it as a brief glimpse of history — Even for those that can’t read the full book, I wanted to make this available to everyone,” explained the Nakamotofamilyfoundation.org website.

Matthew Leising’s published ‘Duality’ hit piece on Bloomberg was quickly forgotten and the second excerpt never came to fruition.

It only took a few hours for armchair sleuths to debunk the exposé’s 21-page manuscript. The document was also assessed with stylometrics and failed to match up with Satoshi’s previous writings. Naturally, the Satoshi Nakamoto autobiography was forgotten about very quickly, the website was deleted, and the second published excerpt never materialized.

Stylometric Research Said Gavin Andresen Was Satoshi

Bitcoin developer Gavin Andresen.

In another case involving stylometry this year, a study was done by the nonprofit organization Zy Crypto, based in England. Stylometry is a scientific method that studies the linguistic style of typed text and handwriting in order to find similarities in prior writings. According to Zy Crypto’s research, the true identity of Satoshi Nakamoto is likely the well-known Bitcoin developer Gavin Andresen. However, after Zy Crypto’s study was published, Andresen spoke out on Twitter and told his followers he had lost a lot of faith in the science of stylometry, stating “My opinion of the accuracy of Stylometry has dropped significantly after reading this.”

The Owner of the Bitcoin Cash Trademark

Another Satoshi sighting took place in June when it was discovered that a resident from Hawaii had filed trademark requests for the name Bitcoin Cash and was also squatting on numerous BCH and Satoshi-based web domains. Two trademark filings for the phrase ‘Bitcoin Cash’ were registered with the United States Patent and Trademark Office (USPTO) in 2018 and the owner of the trademarks also claimed to be Satoshi Nakamoto.

The Bitcoin Cash trademark request was filed by a Hawaiian resident named Ronald Keala Kua Maria.

Looking further down the rabbit hole, the website domains and trademarks led to a person named Ronald Keala Kua Maria. According to reports in 2001, Kua Maria was allegedly involved with fraud and grifting accusations. Kua Maria’s website describes why he patented the phrase ‘Bitcoin Cash’ while also detailing that he is the creator of Bitcoin.

“I am the real one and only Satoshi Nakamoto — I own all the private keys, blockchains, altcoins and bitcoins under copyright law. In the event of my death, incapacitation, coma, kidnapping, detainment and or incarceration all of my copyrighted works and all related works shall no longer be used by anyone anywhere for any reason at any time subject to change without any notice at any time by Ronald Keala Kua Maria only,” explained the website Satoshinakamoto.ws.

A So-Called Block 9 Signature

On Nov. 16, cryptocurrency enthusiasts noticed a message that stemmed from the Bitcoin blockchain at height 9. To some people, the message appeared to be a valid signature from Satoshi’s key in block 9, but the story was also quickly debunked. This particular stunt also involved a Satoshi Twitter handle (now deleted) which tried to spread the disinformation that the signature should be taken seriously.

This Satoshi Twitter handle started spreading the phony signature message on November 16, 2018. Twitter has since deleted this account.

The message tied to block 9 alleged that there are significant problems with the Segregated Witness protocol, but the so-called Satoshi would not reveal the issues until 2019. Then, two well-known blockchain developers Christopher Jeffrey (Purse CTO) and Gregory Maxwell showed the crypto community how the signature was a ridiculous attempt to push an agenda. Maxwell illustrated how easy it was to accomplish this parlor trick and signed a message from the Genesis block. “Are you going to start claiming that I’m the creator of Bitcoin now?” Maxwell asked.

Satoshi Supposedly Says One Word on the P2P Foundation Forum

Another alleged Satoshi message this year came on Nov. 29 when the Satoshi Nakamoto handle registered to the P2P Foundation forum wrote one word. That day the registered user posted the word “nour” which got the internet’s armchair detectives all riled up. The word has several meanings and could translate to an “affectionate and caring person” or it could mean the Arabic version of the word “نور” which is defined as “light.” Aside from Satoshi’s one-word message, the handle of P2P Foundation Satoshi’s last activity was becoming friends with a mysterious person named Wagner Tamanaha back in 2016.

The P2P Foundation forum.

Interestingly, Tamanaha responded to Satoshi’s “nour” message on Dec. 1 in Japanese and stated, “Nice to meet you, thank you very much — Thanks for Bitcoin from Brazil.” The message, which was difficult to translate, was also forgotten quickly, with many people believing that some of Satoshi’s login credentials like his GMX email have been compromised. According to Theymos in 2014, the GMX email sent him a message which made him almost certain that the email account was “compromised.”

The Time Traveling Alien Theory

When the mining pool Btc.top mined block number 528249 on the BTC chain on June 19 with the block hash: 00000000000000000021e800 it drove the internet crazy. The message was first discovered by Mark Wilcox who tweeted the unusual hash to his followers and the message immediately went viral.

The original tweet from Mark Wilcox which drove the internet crazy for a few days.

There were many significant theories tied to the block hash, one of them being that Satoshi could have been a time-traveling alien with extraordinary quantum computing abilities. Twitter personalities discussed how the hash pattern may be tied to ‘E8’, the Theory of Everything, otherwise known as the Unified Field Theory. After intense discussions concerning the meaning of the hash, one Twitter personality stated:

So my mind is melting — Satoshi may be artificial intelligence. And/or time traveling. Maybe quantum computing now exists — Esoteric and metaphysical meaning has found its way to crypto.

The ‘21e800’ message in block 528249 was again forgotten as fast as it came, but remains one of the wildest Satoshi theories of all time.

A Man Called Scronty

Phil Wilson, otherwise known as ‘Scronty.’

Phil Wilson, otherwise known as ‘Scronty,’ claimed to be part of the Satoshi Nakamoto group theory with David Kleiman and Craig Wright. Scronty did a bunch of interviews with news publications this year, including a discussion with news.Bitcoin.com. The huge problem with Scronty’s story is that he has absolutely no evidence that can prove he is legitimately the creator of Bitcoin. But that didn’t stop him from writing his “Bitcoin Origins” story which offers a very long-winded description on how he and two other guys developed the technology. Crypto enthusiasts do not buy Scronty’s story, mostly because he doesn’t have any proof. Martti Malmi, an early developer and one of the older owners of Bitcoin.org, said, it “Never happened. Also: signature or GTFO.” Even during his interview with our publication, Scronty tells us that no one should believe someone is Satoshi without evidence. Scronty emphasized at the time:

Without verifiable proof, no-one can claim to be Satoshi.

Maybe the Hunt for Satoshi Clouds Logic and Reason?

Satoshi sightings and individuals claiming to be Bitcoin’s creator will probably continue in 2019, with the hunt for Nakamoto unlikely to ever end until the inventor is found. The search intrigues a lot of people, and many reporters and amateur investigators have been looking for Satoshi for years. However, the vast majority of the clues, “Easter eggs,” signatures, and individual proclamations have been deemed fraudulent by the cryptocurrency community. Although there are some people who actually believe the odd Satoshi claimant to be legitimate, it’s likely their judgment is clouded by the emotion of wanting to find Satoshi. So far, all of the sightings and self-proclaimed Satoshis have been debunked and have failed to prove anything other than mankind’s proclivity for telling tall tales.

What do you think about all the Satoshi sightings and self-proclaimed Bitcoin creators who appeared this year? Let us know what you think about this subject in the comments section below.

Images via Shutterstock, Twitter, Archive, and Pixabay.

Need to calculate your bitcoin holdings? Check our tools section.

The secondary luxury goods market has been growing wildly in recent years, with more shoppers opting to both sell their lightly used luxury goods like clothing and jewelry for cold, hard cash, as well as buying the pre-owned, authenticated luxury goods of others.

One of the biggest beneficiaries of the trend is The RealReal, a nearly eight-year-old shopping destination for the growing population of people who might not be willing or able to purchase a new Hermes Birkin bag but are willing to buy one in like-new condition for considerably less. The idea — which seems to be working — is to create a virtuous cycle, wherein the bag’s original purchaser receives the bulk of that re-sale price, then uses the money to buy another new handbag (or a used one) that can be resold at a later point in time.

Another beneficiary of the trend: TrueFacet, a five-year-old, New York-based marketplace that claims to have more than 40,000 watches and 55,000 pieces of pre-owned authenticated watches and jewelry for sale at its site, and that has more recently begun offering pre-owned timepieces directly through brands like Fendi Timepieces, Raymond Weil and Roberto Coin that now partner with TrueFacet to carry their pre-owned timepieces with a manufacture warranty.

Apparently, shoppers are buying what they’re collectively selling. The company, which had previously raised $14.7 million in funding from investors, looks to be closing in on another $10 million round, judging by freshly filed SEC paperwork that shows it has so far raised $7 million in funding and is targeting $9.8 million altogether.

TrueFacet has some tough competition in the space, including Crown & Caliber, a six-year-old, Atlanta, Ga.-based company that has never announced outside funding, and 15-year-old, Germany-based Chrono24, which has raised €21 million over the years. Both sell timepieces alone, however.

It also competes directly with The RealReal, which has raised nearly $300 million from investors and sells clothing and high-end home decor, as well as jewelry and watches. (The company doesn’t break out publicly which of these categories outpace the others in terms of sales.)

Interestingly, like The RealReal, which now operates permanent offline stores in both New York and L.A., TrueFacet is also crossing the chasm into the offline world, though it’s taking baby steps toward that end.

Specifically, earlier this month, it announced a partnership with Stephen Silver Fine Jewelry, which sells timepieces to many monied Bay Area VCs and other Silicon Valley bigs at stores in Redwood City and Menlo Park, Calif. For the time being at least, the jeweler will also sell pieces from TrueFacet’s collection.

from Startups – TechCrunch https://tcrn.ch/2ENtCwF

A man with the Surname of Yang has been accused of stealing 100 million Taiwanese dollars (nearly $3.25 million) worth of electricity to mine cryptocurrencies. Yang is suspected of stealing power from 17 different stores in Northern Taiwan to fuel his mining operations.

Taiwanese Miner Steals More Than $3 Million Worth of Power

According to local reports, a Taiwanese man has been taken into custody for allegedly more than $3 million worth of electric power to mine BTC and ETH.

Yang is accused of renting internet cafes or toy stores located on the first floor of a building, before hiring electricians to rewire the power supply to the premises in a way that would prevent the metering of power later diverted to fuel his mining operations. The internet cafes and toy stores would be located on the first floor in order to facilitate Yang establishing a mining rig on the floor above the shop once a new owner had taken over the business.

Wang Zhicheng, the deputy head of the fourth brigade of Taiwan’s Criminal Investigation Bureau, stated: “The group recruited electricians who managed to break into the sealed meters in order to add in private lines to use electricity for free before that usage reaches the meters.”

China Cracks Down on Illegal Mining Operations

Yang was reportedly discovered after Taiwan’s state-owned electricity provider, Taiwan Power Company, became aware of a faulty power supply to a doll shop and subsequently launched an investigation.

Yang is believed to have operated illegal cryptocurrency mines above 17 stores located in the municipalities of Xinbei, Taoyuan, and Hsinchu. The profits generated from Yang’s illegal mining operations are estimated to have been at least 100 million Taiwanese dollars (roughly $3.25 million).

Across the Taiwan Strait, Chinese authorities on the mainland have increasingly taken action against illegal mining operations in recent months. In September, Chinese cryptocurrency miner Xu Xinghua was fined 100,000 Chinese Yuan (roughly $14,500) for stealing electricity from a factory at Kouquan Railway during Nov. 2017 and Dec. 2017 to power 50 cryptocurrency miners that generated approximately 3.2 BTC.

In June, police in China’s Hanshan County arrested an individual for allegedly stealing 150,000 kilowatt-hours of electricity. The miner told police that he had purchased the mining equipment just two months earlier and that he had failed to turn a profit at the time of the arrest.

What is the craziest way to mine cryptocurrency that you have encountered? Share your thoughts in the comments section below!

Images courtesy of Shutterstock

At Bitcoin.com there’s a bunch of free helpful services. For instance, have you seen ourTools page? You can even lookup the exchange rate for a transaction in the past. Or calculate the value of your current holdings. Or create a paper wallet. And much more.

Grove Collaborative, a four-year-old, San Francisco-based startup that sells household, personal care, baby, children’s and pet products, has been busy raising money in 2018, shows two new SEC filings that lists representatives from the company’s earlier investors, including Mayfield, Norwest Venture Partners and MHS Capital, as well as apparent new investor General Atlantic, represented by partner Catherine Beaudoin.

One of the filings shows that Grove Collaborative, which had already raised roughly $62 million as of the start of 2018, subsequently raised $27.4 million more this year. A separate, second filing shows another $76.4 million has been secured in what looks to be a newer round that’s targeting $125 million. It’s a lot of money for such a young company, which suggests it has found traction with a growing customer base.

We’ve reached out to Grove Collaborative and are waiting to learn more.

As we reported back in January, co-founder Stuart Landesberg started the company after working with retail brands during two years as an associate with TPG Capital, which focuses on growth equity and middle-market private equity transactions. With shelf space limited for brands in brick-and-mortar stores, he saw an opportunity for a startup that prompts consumers to buy the kinds of items they buy over and over again just as they are running out of them: think dish soap, pet food, deodorant, vitamins and sunscreen.

Amazon, of course, similarly prompts its customers to buy such items, but Grove Collaborative is marketing to a slightly narrower demographic, that of people who want only all-natural products. In fact, along with the brands that it make it easier for its customers to find — think Method and Mrs. Meyers — the company began selling its own all-natural products this year. Among the many dozens of offerings it now retails under the Grove Collaborative label: a coconut body lotion, a foaming hand soap, coffee filters, soy candles and lip balm.

The move puts the startup in more direct competition with other e-commerce companies, like the consumer goods company Honest Company, which similarly sells natural products for the home and personal care, though many of its products are now sold on shelves in big retail stores like Target.

Grove Collaborative also looks to be competing more directly now with well-funded Brandless, which raised $240 million from SoftBank’s Vision Fund in summer at a valuation of slightly more than $500 million. Brandless also sells its own all-natural household and personal care products, though, unlike Grove Collaborative, it also focuses on food and, unlike Grove, it offers a subscription service, yet does not revolve around one. Grove is exclusively selling an auto-shipment service.

Grove had previously raised two separate rounds of funding in quick succession: a $15 million Series B round it closed in March of 2017, following by a $35 million Series C round it announced in January of this year.

Given that Landesberg was formerly an investor himself, he may well have realized — as have many founders — that raising money next year may be far harder in 2019 than it has been this year. As the CEO of Zymergen, whose giant funding round we recently featured, told Bloomberg last week: “We wanted to have some fat on our bones for sure . . . The time to raise money is when people are giving it to you.”

from Startups – TechCrunch https://tcrn.ch/2QPNYwx

Startups supporting startups are blazing a new trail with support from venture capitalists.

Co-working spaces like The Wing and The Riveter raked in funding rounds this year, as did Brex, the provider of a corporate card built specifically for startups. Now Carta, which helps companies manage their cap tables, valuations, portfolio investments and equity plans, has announced an $80 million Series D at a valuation of $800 million. The company, formerly known as eShares, raised the capital from lead investors Meritech and Tribe Capital, with support from existing investors.

The round brings Carta’s total funding to $147.8 million. Its existing investors include Spark Capital, Menlo Ventures, Union Square Ventures and Social Capital, though the latter didn’t participate in the Series D funding. Tribe Capital, however, is a new venture capital firm launched by Arjun Sethi, who previously led Social Capital’s investment in Carta, Jonathan Hsu and Ted Maidenberg, a trio of former Social Capital partners who exited the VC firm amid its transition from a traditional VC fund to a technology holding company. Tribe is said to be in the process of raising its own $200 million debut fund.

Founded in 2012 by Henry Ward (pictured), the Palo Alto-based company plans to use the latest investment to develop their transfer agent and equity administration products and services to better support startups transitioning into public companies. It also will launch additional products for investors to collect data from their portfolio companies and to manage their back office.

“We’ve come this far by changing how ownership management works for private companies—popularizing electronic securities and cap table software, combined with audit-ready 409As,” Ward wrote in an announcement. “But our ambitions go far beyond supporting privately-held, venture-backed companies.”

Carta, which counts Robinhood, Slack, Wealthfront, Squarespace, Coinbase and more as customers, currently manages $500 billion in equity. This year, Carta expanded its headcount from 310 employees to 450 employees, launched board management and portfolio insights products and completed a study in partnership with #Angels that highlighted the major equity gap female startup employees are victim to.

The study, released in September, revealed that women own just 9 percent of founder and employee startup equity, despite making up 35 percent of startup equity-holding employees. On top of that, women account for 13 percent of startup founders, but just 6 percent of founder equity — or $0.39 on the dollar.

Mark Karpeles, the former chief executive officer of the now-defunct Mt. Gox, has reportedly apologized for the losses that led to the demise of the cryptocurrency exchange. However, the embattled Frenchman insisted on his innocence regarding charges of embezzlement in closing arguments during his trial in Tokyo on Dec. 27.

Karpeles is facing charges of transferring $3 million of client funds to his own account for investment in a software development business. According to prosecutors, who are pushing for a 10-year jail term, the ex-CEO falsified Mt. Gox’s trading system to make customer balances appear healthier than they in fact were.

Karpeles has throughout the period of his trial consistently denied the charges. He claims that the money, moved in the last four months of 2013, was meant to serve as only a temporary loan. He also argued, earlier in the trial, that the funds in question did not belong to clients but were his collapsed company’s revenue.

Appearing in the Tokyo District Court for the closing arguments on Thursday, Karpeles said he was “sorry” for failing to prevent the hack, but insisted on his innocence of the charges he was facing, according to a report by the Japanese broadcaster NHK. Prosecutors aren’t investigating the hack, rather the $3 million alleged embezzlement. The Court is now expected to deliver its ruling, on a case that has run since July 2017, on March 15 next year.

Multi-Million Dollar Theft

Mt. Gox went from handling 70 percent of global bitcoin trades in 2013 to bankruptcy in 2014 after about $480 million was supposedly lost to hackers, with 200,000 bitcoins recovered two weeks later. The current lawsuit is not investigating the cause of this theft.

As the effects of the discrepancy became apparent, the exchange initially delayed withdrawals for up to three months before completely ceasing them altogether, ostensibly over the theft of bitcoins. The company entered bankruptcy proceedings in 2014 but has since undergone civil rehabilitation processes to enable it to pay bitcoin still owed to investors. It has yet to be determined how much users will be repaid, given the numerous fluctuations in bitcoin’s trading price since 2014.

In early December, Japanese prosecutors said they will seek a 10-year jail term for Mark Karpeles over the embezzlement charge. Citing a lack of documentary evidence to support the “temporary loan,” prosecutors argued that Karpeles must be slapped with a harsh sentence for betraying the confidence of investors who trusted him with their money.

“I never imagined things would end this way and I am forever sorry for everything that’s taken place and all the effect it had on everyone involved,” Karpeles said earlier during the bankruptcy saga. Regardless of how the matter plays out in Japan, Karpeles faces more legal trouble in the U.S. where former Mt. Gox clients filed a lawsuit against him several months ago. Karpeles’ lawyers want the lawsuit dismissed on the basis that a U.S. court has no jurisdiction over the matter.

What do you think of the continuing Mt. Gox saga? Let us know in the comments section below.

Images courtesy of Shutterstock.

Need to calculate your bitcoin holdings? Check our tools section.

It’s human nature to see significance in numbers. That’s why the crypto community lost its mind over a block hash containing 18 consecutive zeros earlier this year, and it’s also why there will be great fanfare over Bitcoin’s 10th birthday, despite the fact that numerically speaking, 10 is no more significant than any other integer.

It’s human nature to see significance in numbers. That’s why the crypto community lost its mind over a block hash containing 18 consecutive zeros earlier this year, and it’s also why there will be great fanfare over Bitcoin’s 10th birthday, despite the fact that numerically speaking, 10 is no more significant than any other integer.

Exchanges, wallet developers, P2P platforms and other crypto businesses will be celebrating Bitcoin’s 10th in their own way; expect to see discounts, zero-fee trading and other offers to mark the occasion, plus a whole lot of Bitcoin trivia shared on social media.

Exchanges, wallet developers, P2P platforms and other crypto businesses will be celebrating Bitcoin’s 10th in their own way; expect to see discounts, zero-fee trading and other offers to mark the occasion, plus a whole lot of Bitcoin trivia shared on social media.

One of the biggest stories of 2017 was how initial coin offerings (ICOs) raised billions. 2018 was a different story, with the recurrent themes being regulatory action against ICOs and the majority of these projects failing miserably. In February,

One of the biggest stories of 2017 was how initial coin offerings (ICOs) raised billions. 2018 was a different story, with the recurrent themes being regulatory action against ICOs and the majority of these projects failing miserably. In February,

According to

According to  Yang was reportedly discovered after Taiwan’s state-owned electricity provider, Taiwan Power Company, became aware of a faulty power supply to a doll shop and subsequently launched an investigation.

Yang was reportedly discovered after Taiwan’s state-owned electricity provider, Taiwan Power Company, became aware of a faulty power supply to a doll shop and subsequently launched an investigation.